Which type of mortgage is right for you?

If you have a 20% down payment, we think you'll like our all-in-one mortgage and banking account.

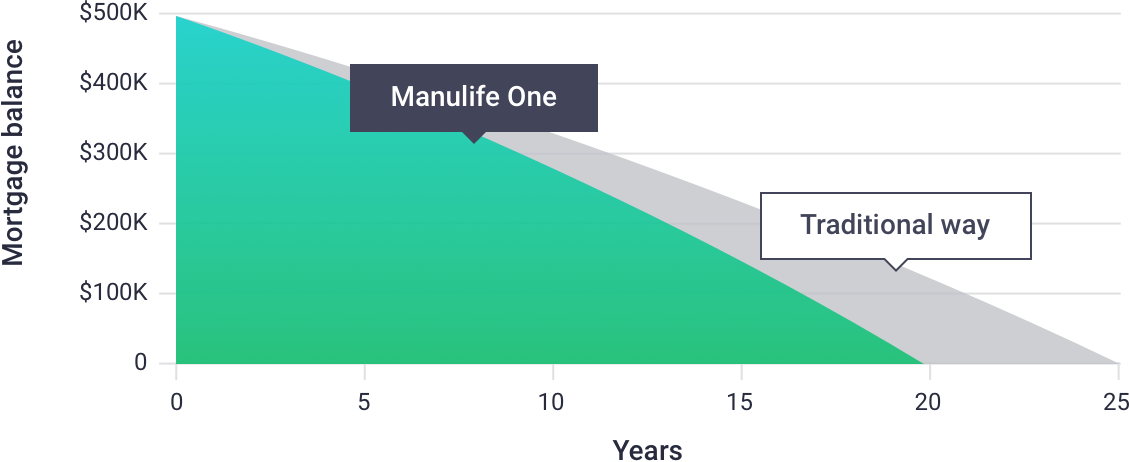

Manulife One

Reduce your interest costs and become debt-free sooner with Manulife One. It’s an all-in-one mortgage that lets you simplify your banking by combining your mortgage with your bank accounts, short-term savings, income, and other debts.

Its flexibility lets you easily increase or decrease your mortgage payments as your goals change and you’ll enjoy convenient access to your home equity when a need arises.

Manulife One is right for you if you’re buying a home and have at least a 20% down payment, or if you want to refinance or transfer in your existing mortgage and have at least 20% equity in your current home.

We think you'll like our flexible mortgage with a high interest chequing account.

Manulife Bank Select

Customize your mortgage, your way with Manulife Bank Select. It lets you divide your mortgage into different portions, each with its own amount, interest rate and term. You can choose the payment schedule for each portion that works best with your budget.

It also brings your banking together with a high-interest chequing account to go along with your mortgage. You’ll enjoy free banking, unlimited transactions and a high interest rate chequing account when you maintain a minimum balance of $5,000.

Manulife Bank Select is right for you if you’re buying your first home and have at least a 5% down payment or want to switch, refinance or renew your current mortgage.

Mortgage calculators

FAQ

Getting mortgage pre-approval should be your first step when buying a home. A pre-approval lets you know how much the bank is willing to lend and gives you an idea of your estimated monthly payments. This allows you to focus your search on homes within your approved price range and make an offer without worrying about whether you’ll be able to get financing.

You can buy a home with as little as 5% of the total purchase price of the new home, which means you can borrow up to 95% of the value of the home. The amount of your down payment will determine what kind of mortgage you qualify for.

- If you have a down payment of less than 20%: you’ll need a high ratio mortgage. With this type of mortgage, you’ll need to purchase mortgage default insurance. The cost of default insurance can be added to your mortgage or paid in a one-time payment.

- If you have a down payment of 20% or more: you can have a conventional mortgage. With a conventional mortgage, there’s no need to purchase mortgage default insurance.

Your amortization is the length of time it will take you to pay off your entire mortgage at your current interest rate and payment. Your amortization will change over time as you renew at different interest rates, with different payment amounts.

For example, you might have a five-year, fixed-rate mortgage with an amortization of 25 years. This means the life of the mortgage (amortization) is 25 years and your interest rate and payments are guaranteed for the five-year term. After five years you’ll have 20 years left on the life of your mortgage and you can renew the interest rate for another term, for example another five years.